Q2 2026 Market Commentary

From Shock to Recovery

The second quarter of 2026 delivered one of the strongest quarterly performances for U.S. and global equity markets since the post-pandemic rebound of Q2 2020, marking a sharp reversal from the volatility and losses that characterized the first quarter. After a difficult start to the year, markets rebounded sharply as the U.S. Iran conflict, which had disrupted global energy markets and driven a spike in the CBOE Volatility Index (VIX) during Q1 moved toward de-escalation. News flow was often volatile, with reports of progress frequently interrupted by renewed tensions or conflicting comments, but as the probability of resolution improved and negotiations advanced, commodity prices retreated from their highs, easing concerns around both higher inflation and weaker global growth.

The economy proved more resilient than many anticipated. Consumer spending continued to expand, labor market conditions showed some signs of improvement, and technology capital expenditure remained strong. The combination of resilient demand and easing energy pressures shifted the balance of risks toward a more constructive backdrop by quarter-end.

The Numbers

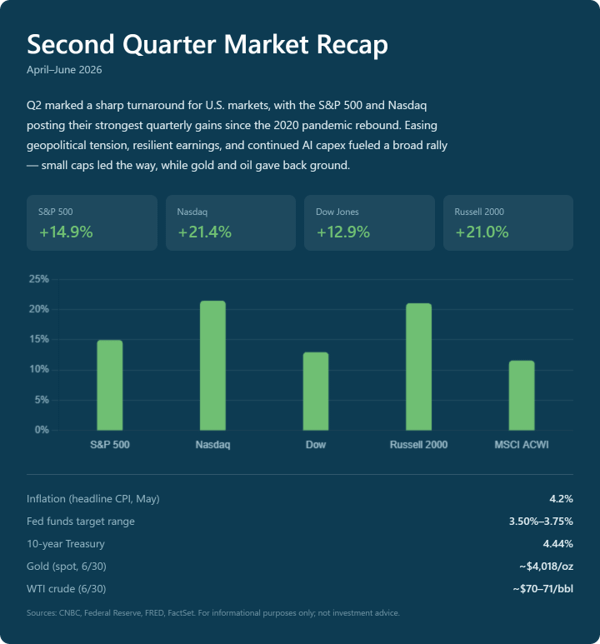

The S&P 500 and Nasdaq each turned in their best quarter since Q2 2020 — up roughly 15% and 21%, respectively — and the Dow had its strongest showing since Q4 2022, up roughly 13%. Early gains were concentrated in mega-cap growth and tech, but small-cap, micro-cap, and value benchmarks all reached new record highs by quarter’s end alongside it. The Russell 2000 posted its best first half since 1991, up more than 21% year-to-date.

Equities significantly outperformed fixed income this quarter as investors looked through near-term geopolitical uncertainty and focused on earnings fundamentals. Corporate profit growth trended strongly across most major regions, which let equities generate outsized returns without a significant increase in valuation multiples. The AI buildout remained the defining theme, persistent shortages in semiconductors and memory components, paired with continued growth in tech investment, drove exceptional performance in AI-linked markets. But the advance was broader than that, financials, banks, and small-caps also posted strong gains, and nearly every U.S. large-cap sector outside energy and utilities finished the quarter in positive territory.

A New Fed Chair, and a Rate Hold

The quarter also brought a genuine changing-of-the-guard moment at the Fed. Kevin Warsh was confirmed by the Senate 54-45 on May 13 and ran his first FOMC meeting as Chairman on June 17th. The Committee’s decision was a non-event by design, rates held at 3.50% – 3.75%, unanimous 12-0. First meetings under a new chair are usually about signaling continuity before setting a new direction, and that’s exactly the read here.

Inflation: Hot Headline

Inflation is where the quarter gets more technical. May CPI ran 4.2% year over year, the highest print since April 2023, driven largely by the lagged pass-through of higher energy prices tied to the Iran conflict. Core CPI told a different story, holding at a comparatively moderate 2.9%. Producer prices accelerated further, up 6.5% year-over-year in May, the fastest pace since late 2022.

Growth Held Up Better Than the First Read Showed

The final estimate for Q1 2026 GDP was revised up to a 2.1% annualized rate, well above the 1.6% second estimate. A meaningfully stronger economy than the market was pricing in earlier in the year, and a major driver behind why the rebound sustained momentum once geopolitical concerns eased.

Global Central Banks: Less Dovish

Outside the U.S., the policy path was more mixed, but most major central banks entered the second half of the year with a more restrictive stance than where they started 2026. The ECB and Bank of Japan were among the central banks delivering rate increases during the quarter, and forward guidance is expected to play a smaller role in communications broadly going forward.

The Takeway

Q2 2026 closed out one of the strongest quarters for U.S. and global equities since the 2020 rebound, as easing geopolitical tension and resilient corporate earnings more than offset a hot inflation backdrop and a hawkish turn at the Fed. The rally broadened well beyond mega-cap tech by quarter’s end, with small-caps, value, and cyclical sectors all sharing in the gains alongside AI-linked names. Heading into the second half, the path forward hinges on two things, whether inflation keeps cooling as energy prices normalize, and how the new Fed under Chairman Warsh navigates a policy stance that’s shifted from cutting to weighing a hike, even as global central banks broadly move toward tighter policy. For now, the market has given investors permission to look past the noise — the second half will test that confidence.

This material is provided for informational purposes only and should not be construed as investment advice, a recommendation, or an offer to buy or sell any securities. The views expressed herein are those of the author as of the date of publication and are subject to change without notice based on market and other conditions.

All investments involve risk, including the potential loss of principal. Past performance is not indicative of future results. There can be no assurance that any investment strategy will be successful.

The information contained herein has been obtained from sources believed to be reliable, but its accuracy and completeness are not guaranteed. Any forward-looking statements or projections are based on current assumptions and expectations and are subject to change. Actual results may differ materially.

References to specific asset classes, sectors, or market developments are for illustrative purposes only and should not be considered a recommendation to invest. Diversification does not guarantee a profit or protect against loss in declining markets.

Fixed income investments are subject to interest rate risk, credit risk, and inflation risk. Equity investments are subject to market volatility and company-specific risks. Investments in international and emerging markets may involve additional risks, including currency fluctuations, political instability, and less developed regulatory environments.

This communication is intended for a broad audience and does not take into account the specific investment objectives, financial situation, or needs of any individual investor. Investors should consult with their financial advisor before making any investment decisions.

Benchmark Wealth is a Registered Investment Advisor. Registration with the SEC or any state securities authority does not imply a certain level of skill or training.