Retirement & College Planning

Trump Accounts: What They Are, and Whether One Belongs in Your Family's Plan

Matt Eltringham

Managing Director, Wealth Advisor

My wife and I recently welcomed our daughter into the world, and like a lot of new parents, one of my first instincts was to start thinking about her future. When a new savings vehicle shows up — one where the government contributes money toward your child’s account — I wanted to look at that closely, as both an advisor and a dad.

In this article, we’ll answer the most common questions about Trump Accounts, compare them with a 529 plan, and help you decide whether one fits your family’s broader financial strategy.

As with any planning decision, the right answer depends on your family’s goals, tax situation, and time horizon. There are real advantages here — including free seed money for eligible children from Uncle Sam — but there are also meaningful restrictions, and understanding both is crucial to make an informed decision.

What Is a Trump Account?

A Trump Account (formally a Section 530A account, created under the One Big Beautiful Bill Act) is a new type of tax-advantaged account for children — essentially a traditional IRA opened for a minor. An authorized adult — generally a legal guardian, parent, adult sibling, or grandparent, in that order — can open one for any child under 18 with a valid Social Security number.

The headline generating quite a bit of buzz is the $1,000 in seed money: children who are U.S. citizens and born between January 1, 2025, and December 31, 2028, are eligible for a one-time $1,000 contribution from the U.S. Treasury when the account is elected on IRS Form 4547. Free money from the government toward your child’s future? For eligible families, that alone is worth the paperwork.

A few operational facts to anchor expectations:

- Accounts can be set up now, but no contributions of any kind can be made until July 4, 2026 — including the $1,000 seed.

- Contributions are not tax-deductible. Money goes in with after-tax dollars.

- Growth is tax-deferred, not tax-free. Earnings aren’t taxed while they stay in the account, but they are taxable when withdrawn.

- The funds are locked in for the long term. No withdrawals are permitted during the “growth period,” which runs generally through December 31 of the year the child turns 17. On January 1 of the year the child turns 18, the account converts to a traditional IRA and normal IRA rules take over.

This is fundamentally a long-term, retirement-oriented vehicle — not a flexible, all-purpose or emergency savings account.

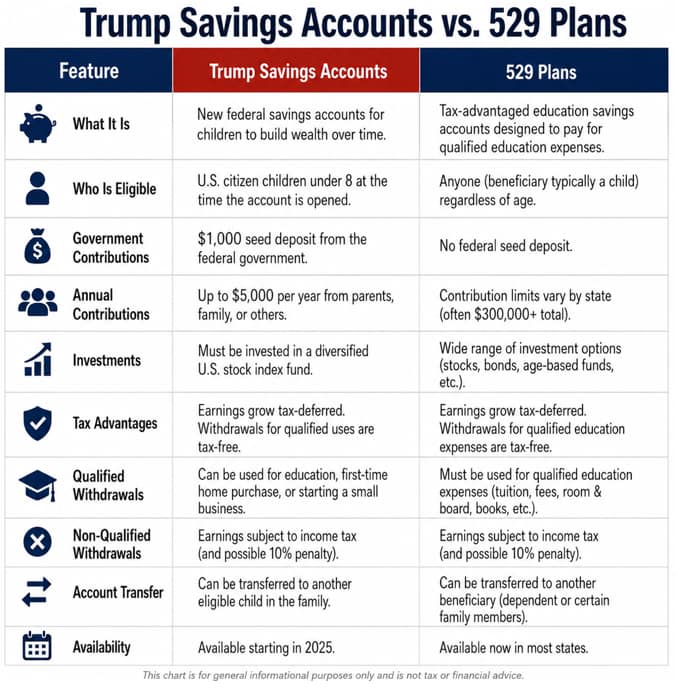

Trump Savings Account vs. 529 Plan

When evaluating a Trump Account vs. 529 Plan, it’s important to understand the key differences. Both offer tax advantages but serve different financial goals.

The practical takeaway: if your primary goal is education, a 529 generally offers stronger, more targeted tax benefits and far more flexibility, and it’s often the more efficient dollar. The Trump Account’s distinctive edge is the $1,000 of free money for eligible children and its role as an early, long-horizon retirement-style account. For many families, the answer isn’t one or the other — it’s capturing the seed money while continuing to use the tool best suited to each goal.

What About A Roth IRA?

Parents often ask why not simply open a Roth IRA for their child instead. The obstacle is that a Roth IRA can only be funded with the child’s own earned income — a baby or young child who isn’t working has nothing eligible to contribute, so a Roth generally isn’t on the table in the early years. A Trump Account carries no such requirement: an adult can open and fund it even if the child has never earned a paycheck. That’s a real gap it fills, giving a child a tax-advantaged investment account years before a Roth IRA would even be an option.

The Roth planning component resurfaces later, and it may be one of the most valuable planning opportunities the account creates. Because a Trump Account becomes a traditional IRA when the child turns 18, your now-young-adult can convert some or all of it to a Roth IRA over time. The ideal window is often early adulthood, while they’re in the early career years and sitting in one of the lowest tax brackets they’ll ever occupy. Converting then means paying the tax on the conversion at a low rate — after which the money can keep growing and eventually be withdrawn tax-free for the rest of their life. Handled thoughtfully, a modest account seeded near birth can grow into a long-running, largely tax-free retirement asset.

One catch to plan around if you’re eyeing that conversion during the college years: the kiddie tax. If your child converts while they’re still in school, the taxable portion of the conversion could count as unearned income—and that can trigger the kiddie tax, which often means being taxed at the parent’s rate. That can quietly undo the very low-bracket advantage you were converting to capture. Because the kiddie tax stops applying in the year the child turns 24, the real sweet spot for a sizable conversion is often once they’ve aged out of it or are supporting themselves independently.

Is Trump's Savings Account Strategy Right for You?

Every family’s situation is different, so there’s no one-size-fits-all answer. For eligible children, the $1,000 seed contribution is close to a no-brainer — it’s free money that compounds for years before anyone can touch it. Beyond that, whether to contribute further depends on how a locked-in, retirement-oriented account fits alongside your 529 plans, custodial accounts, and other goals.

Weigh the benefits — free seed money, tax-deferred growth, employer contributions — against the tradeoffs: a modest annual limit, restricted investments, no access until adulthood, and ordinary-income tax (plus possible penalties) on withdrawals. If you’d like to talk through how a Trump Account fits into your family’s long-term plan, schedule a meeting with me or one of our wealth advisors here.

FAQs

It's a new tax-advantaged savings vehicle created under Section 530A of the tax code — effectively a traditional IRA opened for a child. It's designed to encourage long-term saving and investing for the next generation, seeded (for eligible children) by a one-time $1,000 federal contribution. It is a long-horizon, retirement-oriented account, not a flexible or emergency-access one.

Both are tax-advantaged, but they serve different goals. A 529 is purpose-built for education, offers tax-free qualified education withdrawals, often carries a state tax deduction, and has much higher contribution room. A Trump Account is oriented toward long-term/retirement savings, offers only tax-deferred growth, and taxes distributions like a traditional IRA. If education is your priority, a 529 is usually the stronger tool; the Trump Account's standout feature is the $1,000 of free seed money for eligible children.

Contributions are not deductible, but earnings grow tax-deferred until withdrawn. Form 4547 is the IRS election form used to open the account and, for eligible children, to request the $1,000 pilot contribution. You can file it with your 2025 tax return (electronically or on paper) or through TrumpAccounts.gov. It also identifies the responsible party who manages the account until the child turns 18.

For families, the accounts offer tax-advantaged growth, flexibility for future education costs, and penalty-free access for emergencies—features that can support evolving needs as children grow. They’re designed for easy digital management and often come with financial literacy resources to help parents and kids build strong saving habits together.

File Form 4547 with your 2025 tax return or at TrumpAccounts.gov; you'll need the child's name, date of birth, Social Security number, and relationship. At launch, accounts are custodied through the U.S. Treasury program, and once activated you can track contributions and balances through the official Trump Accounts app. It's most compelling if your child qualifies for the $1,000 seed money and you're comfortable with a long-term, restricted account. Weigh it against a 529 and other options, and consider your goals, time horizon, and state tax situation before deciding.

This material is provided for informational purposes only and should not be construed as investment advice, a recommendation, or an offer to buy or sell any securities. The views expressed herein are those of the author as of the date of publication and are subject to change without notice based on market and other conditions.

All investments involve risk, including the potential loss of principal. Past performance is not indicative of future results. There can be no assurance that any investment strategy will be successful.

The information contained herein has been obtained from sources believed to be reliable, but its accuracy and completeness are not guaranteed. Any forward-looking statements or projections are based on current assumptions and expectations and are subject to change. Actual results may differ materially.

References to specific asset classes, sectors, or market developments are for illustrative purposes only and should not be considered a recommendation to invest. Diversification does not guarantee a profit or protect against loss in declining markets.

Fixed income investments are subject to interest rate risk, credit risk, and inflation risk. Equity investments are subject to market volatility and company-specific risks. Investments in international and emerging markets may involve additional risks, including currency fluctuations, political instability, and less developed regulatory environments.

This communication is intended for a broad audience and does not take into account the specific investment objectives, financial situation, or needs of any individual investor. Investors should consult with their financial advisor before making any investment decisions.

Benchmark Wealth is a Registered Investment Advisor. Registration with the SEC or any state securities authority does not imply a certain level of skill or training.