4th Quarter 2025 Market commentary

Resilience Through Uncertainty

As 2025 came to a close, markets delivered a reassuring message: even with plenty of uncertainty, the underlying trend remained constructive. The fourth quarter was shaped as much by what investors couldn’t see as by what they could. A record 43-day U.S. government shutdown delayed key economic data just as investors were looking for confirmation on growth, inflation, and interest rates.

Despite that fog, risk assets proved resilient. Global growth held up, inflation continued to cool gradually (though it remained above central bank targets), and policymakers around the world leaned toward easier, not tighter, financial conditions. The result was a solid finish to a strong year across most asset classes.

The Big Picture: "Good Enough" Was Enough

The macro backdrop in late 2025 could best be described as good enough. The U.S. economy continued to expand, supported by steady consumer spending and a gradually cooling but still healthy labor market. Inflation stayed sticky in areas like shelter and services but avoided re-accelerating, giving central banks room to ease.

In the U.S., the Federal Reserve cut interest rates twice during the quarter, bringing the federal funds rate into the mid-3% range. While some policymakers expressed concern about cutting too far, the overall message was clear: downside labor-market risk mattered more than squeezing out the last bit of inflation.

Internationally, the tone was also supportive. Europe showed modest growth despite ongoing political uncertainty, Japan continued its slow exit from ultra-easy policy, and many emerging markets benefited from stabilizing trade conditions and a manageable U.S. dollar.

Importantly, tariff concerns, which loomed large earlier in the year, proved less disruptive than feared. Actual tariff collections rose but remained well below levels implied by announced policies, suggesting exemptions, negotiations, and implementation delays softened the real-world impact.

Market Performance: A Strong Finish to a Strong Year

Financial markets closed out 2025 on solid footing. Equities and bonds both posted gains in the fourth quarter, and most asset classes ended the year with positive momentum.

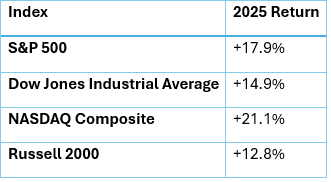

Equity Market Returns

Non-U.S. equities outperformed U.S. markets during the quarter, even as the U.S. dollar strengthened modestly. Developed international and emerging markets both finished the year with strong double-digit returns, benefiting from improving growth expectations and easing financial conditions.

In the U.S., equity gains were positive but more measured. Performance was broader than in prior years, though leadership remained selective.

U.S. Equity Snapshot

While mega-cap technology stocks continued to play an important role, their contribution to total market returns declined compared to 2023–2024. This shift reflected investors becoming more selective, particularly around artificial intelligence (AI) investment and profitability.

Sector Performance: Dispersion Matters

Sector leadership during the quarter reinforced the importance of diversification and fundamentals.

Health care stood out as the top performer in the quarter, while real estate and utilities lagged amid higher long-term interest rates and lingering concerns around commercial property fundamentals. Leadership remained relatively narrow, underscoring the value of selective exposure rather than broad sector bets.

Fixed Income: Income Finally Felt Like Income Again

Fixed income investors also had reason to be encouraged. The Fed’s rate cuts helped support bond prices, particularly at the front end of the yield curve.

- The 2-year Treasury yield fell to about 3.47%

- The 10-year Treasury yield ended the quarter near 4.17%

This dynamic led to a modest steepening of the yield curve. Investment-grade and high-yield credit both posted gains of around 1% during the quarter, with spreads remaining near their tightest levels of the year.

Credit fundamentals remained healthy, though AI-related capital expenditures contributed to higher corporate debt issuance, a trend investors will continue to monitor.

Real Assets: Metals Shine, Real Estate Lags

Real assets delivered mixed results.

- Natural Resources rose nearly 7%, driven by strong gains in metals.

- Gold climbed roughly 12% in the quarter.

- Silver surged more than 50%, supported by industrial demand and investor interest.

- Global Real Estate slipped slightly, weighed down by office and data-center challenges.

These trends reinforced the role of real assets as diversifiers rather than uniform inflation hedges.

AI: From Excitement to Scrutiny

Artificial intelligence remained a central theme throughout the quarter, but the narrative evolved. Early enthusiasm around massive AI investment plans gave way to tougher questions about returns, cash flows, and financing needs.

While many large technology companies maintain strong balance sheets and profitability, investors increasingly differentiated between likely long-term winners and companies facing execution risk. This shift contributed to wider dispersion within both mega-cap tech and the broader AI ecosystem.

Economic Signals: Strong Data, Cautious Sentiment

Economic data continued to show resilience. U.S. GDP growth exceeded 4% in the third quarter, and estimates for the fourth quarter pointed to continued expansion, albeit at a slower pace.

At the same time, consumer confidence remained subdued. Surveys reflected ongoing concerns about inflation, interest rates, and political uncertainty even as actual spending stayed relatively strong. This gap between “hard” and “soft” data became a defining feature of late 2025.

Looking Ahead to 2026

As investors head into 2026, the environment remains supportive but more nuanced. Easier monetary policy and solid earnings growth provide a foundation for continued opportunity, but the margin for error has narrowed.

Key themes to watch include:

- The pace and extent of future rate cuts

- Labor-market trends as growth cools

- Corporate earnings delivery in a higher-cost capital environment

- Ongoing geopolitical and policy risks

In this setting, markets are likely to reward discipline over speculation. Diversification, thoughtful security selection, and a focus on durable cash flows matter more than chasing headlines.

As always, periods like these tend to favor investors who stay patient, forward-looking, and aligned with long-term objectives rather than short-term market noise.

Moving into 2026, we’re here to help ensure your financial strategy stays aligned with your goals in a market shaped by steady growth, shifting interest rates, and more selective opportunities. Whether it’s positioning your portfolio to participate in areas of strength or managing risk amid ongoing uncertainty, we’re happy to navigate what’s ahead together. Please don’t hesitate to reach out if you have questions or want to talk through how these themes apply to your own situation, we’d love to connect.

Nothing contained herein shall constitute an offer to sell or solicitation of an offer to buy any security. Material in this publication is original or from other sources published with express permission and is believed to be accurate. However, we do not guarantee the accuracy or timeliness of such information and assume no liability for any resulting damages. Readers are cautioned to consult their own tax and investment professionals with regard to their specific situations.

Copyright © 2025 FMeX. All rights reserved.